Adieu, New College

The Florida House and Senate appear to have a deal to sell the USF Sarasota-Manatee campus to New College. New College will get the real estate and the buildings and the debt. USF maintains the students and has priority access to facilities until the students are taught out or transfer.

As I noted back in December when DeSantis first released the budget, New College is acquiring the primary liability of this regional USF campus without acquiring the primary asset. And I do use the terms “sell” and “acquire” because the price of the deal is the debt that New College is agreeing to assume.

(Note: The exact debt is generally assumed to be $53M, but that hasn’t been confirmed. USF has bonds and other debt for that campus for varying amounts, so it’s possible the number is lower. All debt-rates below are institutional per FTE.)

For over a decade, New College has been frozen out of the credit markets because its per capita debt was nearly double the SUS average, and its tuition revenue was anemic.

Since 2022, New College’s tuition has essentially fallen to $0.

After this acquisition, New College’s institutional debt will be about $70M. To put that in perspective, with its current $17M in debt, the college’s per-FTE debt – while bad enough to freeze it out of the debt markets – wasn’t even in the top 100 for public colleges in the U.S.

With an additional $53M in debt, New College has about $78k/debt/student and moves from outside of the top 100 to the 13th most-indebted per FTE public college in America. Of small public colleges, New College moves up to second place, behind University of Puerto Rico-Utuado.

Or to put it another way, there is no small public college in any U.S. state with more per FTE debt. And the reason for that is simple: they can’t afford it.

Only one of the top-20 debt-per-FTE public colleges is financially stable (UVA). All of the rest show moderate or substantial signs of financial stress (closing programs and branch campuses, laying off personnel).

I’ll discuss debt in a bit more detail in another post, but it’s worth pointing out a few distinctions between debt in private and public colleges. First, most private colleges are capable of carrying significantly more debt because they drive significantly greater tuition revenue. Public colleges become financially unstable at far lower debt levels (or just become wards of the state, essentially). Second, while most of the high-debt public colleges are financially stressed, most of the high-debt private colleges are not. The common pattern among those colleges is marketing pricing power; their brand enables them to get out of financial problems. Note that the only low-stress/high-debt public college, UVA, also has pricing power. (For public colleges, ‘pricing power’ generally means out-of-state pricing power.)

So, the singular solution for maintaining financial stability despite high debt is pricing power. (No, it’s not the endowment.)

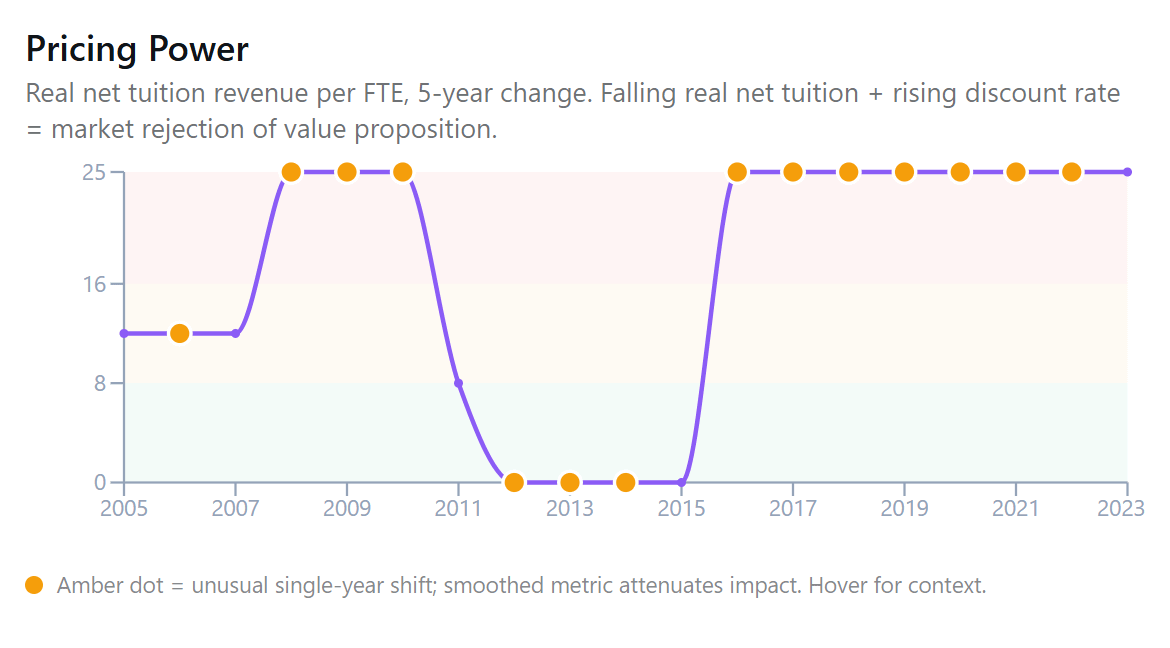

This is crucial because, as noted above, New College has no demonstrated pricing power in the market. I could remind you of this:

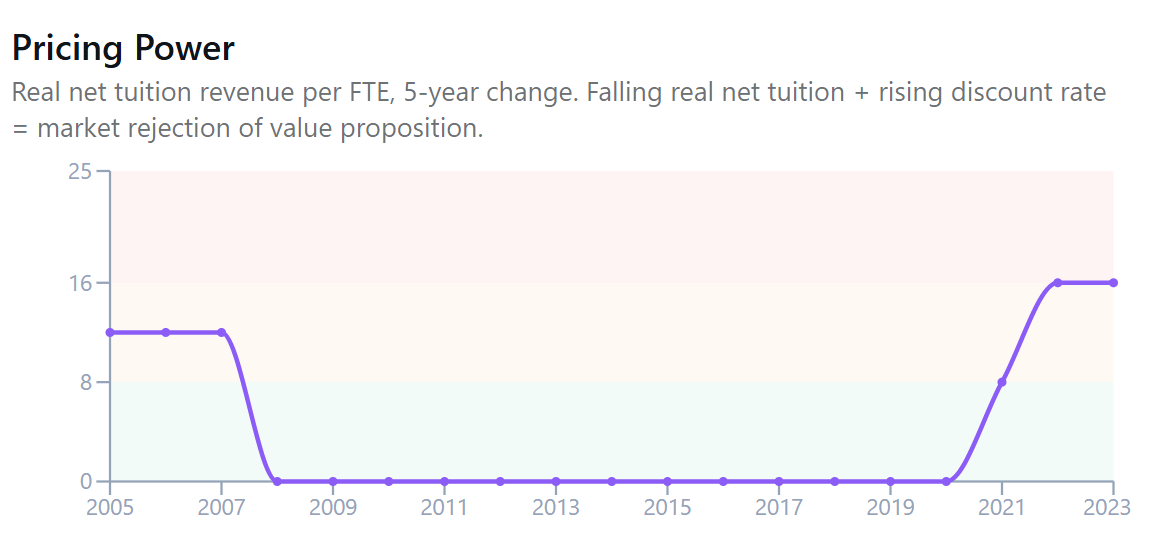

By comparison, while New College has a decade-long streak of no-pricing power (max score of 25 = min pricing power), UVA ran more than a decade at max pricing power.

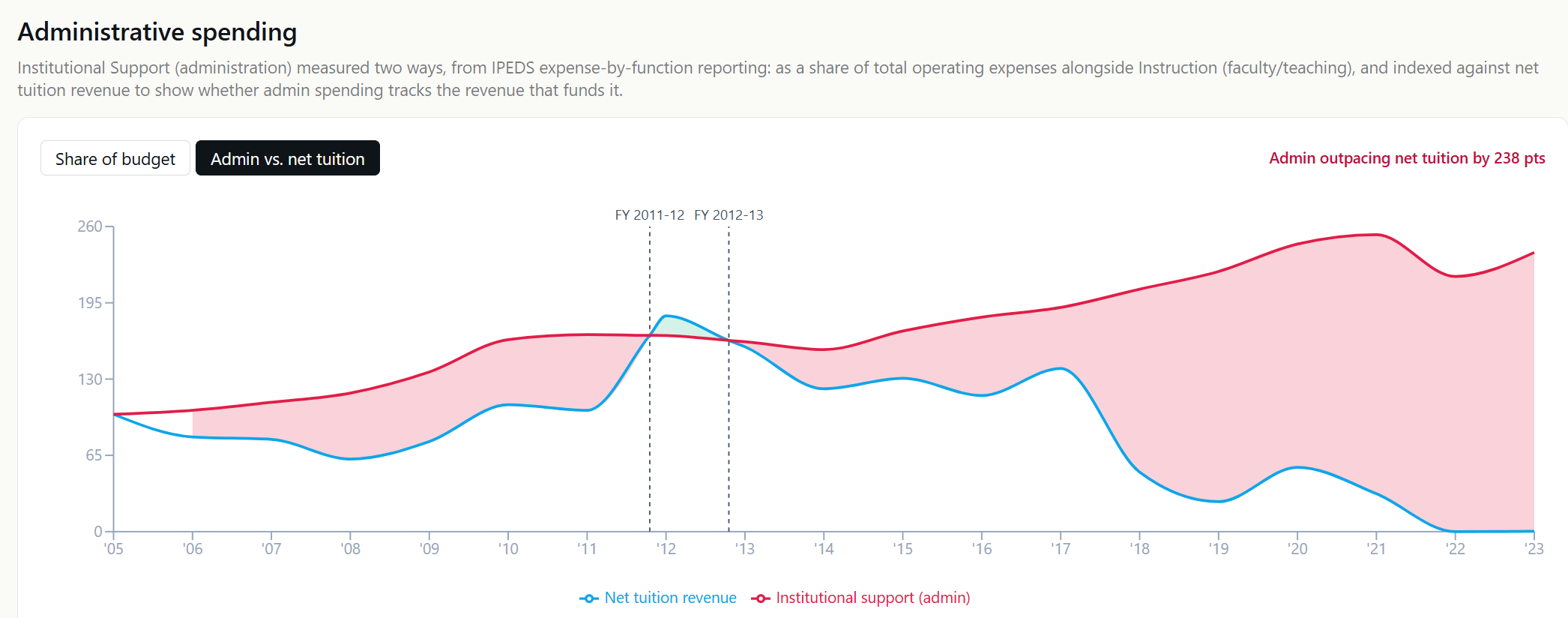

Or, I could remind you of New College on the expense side:

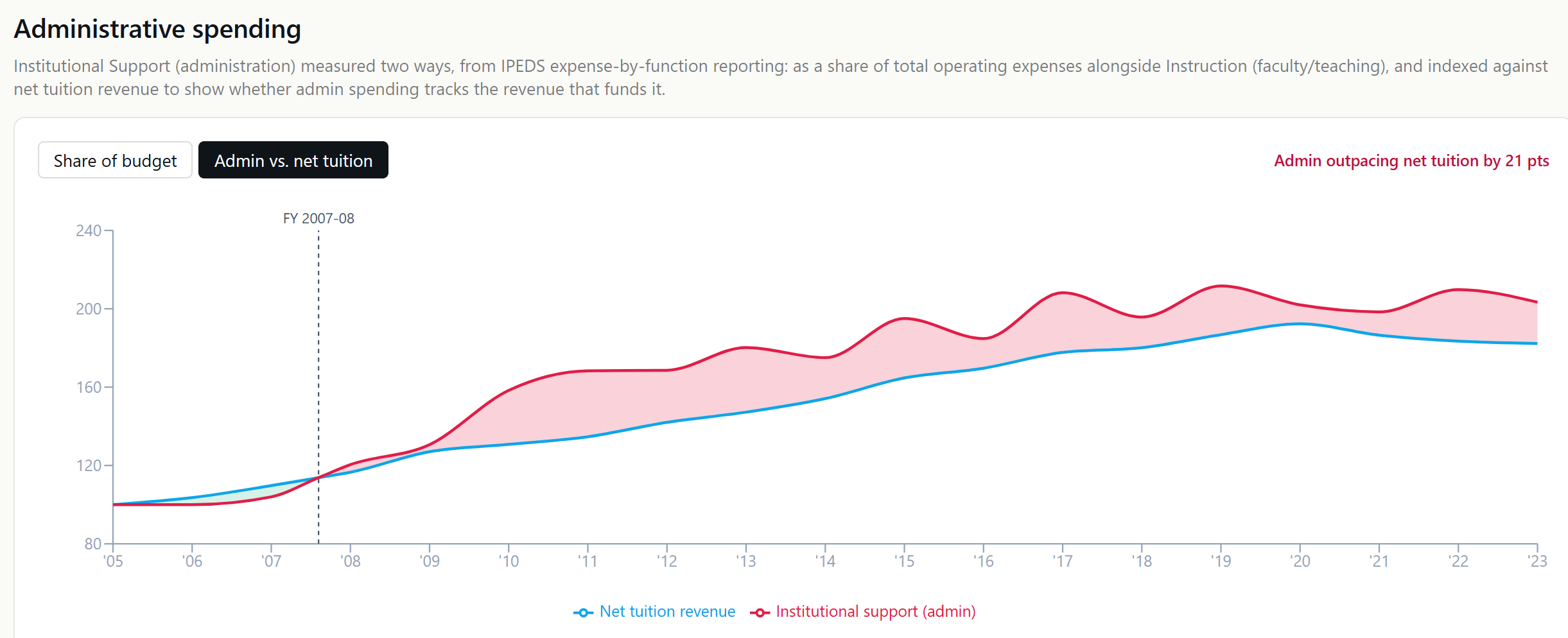

How ridiculous is that? Again, UVA:

Speaking of tuition, this cracks me up:

That’s not in hundreds or thousands; that’s just dollars. For 2022-23, New College’s net tuition per FTE was $10. Take that to the bank and see what you can borrow.

Same metric, same year, UVA:

I use UVA as an example because it’s the only top-20 debt-per-FTE public college that is financially stable. Its pricing power and real tuition revenue — all fueled by brand — enables it to maintain financial stability despite its out-sized debt. Now that New College will be on the top-20 debt list, we should ask: does New College have that level of in-market brand?

The New College president claims he can “find” the $2M/year in carrying charges and seemingly is ignorant of the new operating costs he’s assuming. Does the USF campus power itself? Is the mulch free? Are the insurance carriers luxuriating you with $1/year policies? That USF campus had operating expenses of about $20M/annual (about $35M-$39M total/annual expenses). It may be possible to operate it on $10M. It’s not possible to operate it on the president’s proposed $0.

Hence the initial House proposal for the transfer included $23M in additional funding; that’s about what one needs to operate the campus (not operate a college – just a campus).

The singular concession to which the Senate agreed is to relax the language around the usual $5M-$6M the legislature provides the college for scholarships. Of note, that money was about 100% of the college’s tuition revenue (in addition to ~$10M in aux revenue).

New College has for many years had a rather tumultuous relationship with Tallahassee, including in the last few years (note that the president has never received his priority ask from the legislature). This time was different because USF wanted to relieve itself of this substantially non-performing $53M in debt.

Relieving oneself of $53M in debt against no revenue would require locating an idiot with sufficient financial illiteracy as to think that this deal is somehow non-lethal. But the moment that Tallahassee sobers up, I strongly suspect things will be rather ugly for New College.

And this essentially kills any effort to take the college private. (New College’s current max revenue of about $17M, against $17M in debt, wasn’t great but is workable. Max revenue of $17M against $70M in debt is not feasible in the private world, which requires some degree of sanity.)

Curiously, I haven’t seen anything regarding the financial instrument that will be used for New College to assume this debt. If this were a market-based deal, New College would need to access the credit markets directly. But, I suspect, the instrument will be a note between New College and USF. The New College president will sell that as being the “easy” and “obvious” way to conduct this transaction, but USF will still hold the liability on the bonds (which means this isn’t USF’s preferred instrument). A deal financed with a private note signifies that New College could not go to the credit markets itself. The instrument itself may indicate exactly how bad this deal is for New College.

This is exactly the kind of financial instability the college didn’t need. Miracles can happen – and, assuming the financial instrument above, New College will have USF lobbying in Tallahassee to ensure that New College receives sufficient funds to pay USF – but a struggling college larding up on debt is typical end-stage behavior.

(So what happens? New College defaults in 3-5 years; historically, default is usually 5-10 years after such a deal closes, but this one is unusually bad. USF assumes the property. Tallahassee approves closure. The real estate is auctioned. It’s worth noting that for most colleges, the primary asset is not the real estate. Creditors do not want to foreclose on academic buildings and student centers. And, often, the real estate is worth less than the debt. Most college’s primary assets are their revenues — mostly, tuition revenues. New College is not most colleges.)

The obvious irony here is that in 1975 USF acquired New College’s campus and debts to keep private New College from closing. Now in 2026, New College will acquire USF’s debts to keep it from … well, I don’t know what would have happened if Sarasota Manatee USF had continued on. I think this is a continuation of Bob Allen’s plan to destroy the village in order to save it.

I have four questions.

First, the author writes, "New College has for many years had a rather tumultuous relationship with Tallahassee, including in the last few years (note that the president has never received his priority ask from the legislature)." What is the priority ask that the legislature has never given President Corcoran?

Second, President Corcoran's contract concludes in late February, 2028. The author estimates that New College may default on the debt it is assuming in three-to-five years. I suppose that prior to the default, the college will experience financial distress that will become evident in different ways. Any informed speculation about what form the distress might take? Or about how it might affect Corcoran's final two years or the search for a successor to Corcoran? (I assume Corcoran will not want to renew his contract if it becomes clear the college is undergoing a rapid financial decline.)

Third, the author writes, "The singular concession to which the Senate agreed is to relax the language around the usual $5M-$6M the legislature provides the college for scholarships. Of note, that money was about 100% of the college’s tuition revenue (in addition to ~$10M in aux revenue)." I believe that the college's growth in undergraduate enrollment (Corcoran's one substantive accomplishment) has been driven by handing out generous scholarships to students with little regard for academic merit or preparation. If the terms of the deal include allowing the college to use money that has been earmarked for scholarships in other ways, will Corcoran still have sufficient funds to attract increasing numbers of students to New College?

Fourth and finally, Governor DeSantis championed this deal. Corcoran may be unwise in financial matters, but what about the Governor and those around him? Might there be more to the story than meets the eye? Might there be some manner in which New College could handle the debt that isn't obvious? I know DeSantis will be gone soon, but would he deliberately set up his pet project for financial collapse in three-to-five years? Answering these questions may go beyond whatever empirical evidence is available at the moment, but I think the questions are worth posing.